How Machines Beat Human Investors

Why do stocks markets go up and down? Traditional theories are due an update in the machine learning age. It’s time to take The Sniff Test.

A Good Explanation

An explanation is a hard to vary theory for why things happen. It encompasses the best of our knowledge but is neither definitive nor final. New knowledge will be discovered that updates and improves our explanations. This is progress.

Definitions also change. Ancient Greeks said the atom was indivisible, but we know this is wrong. Arguing that atoms can’t exist because splitting them contradicts the Greek definition, is nonsensical. Definitions evolve with our understanding.

People who want to sound clever ask you to define your terms. “What do you mean by that?” they’ll say. Word games are not knowledge and progress requires flexible thinking.

Free will is an example. As there is a mechanical explanation for things – particle A collides with particle B causing C – some say free will cannot exist. But it’s much better to have a looser meaning of free will, than to deny control over your life. Supposedly smart people get this wrong all the time.

Philosophy is taught as word games. It should be the search for better explanations and a precursor to new knowledge. Science means coming up with new, hard to vary explanations that may be tested. It starts with creating ideas, which is philosophising.

If definitions can change does that mean people can change gender? Yes, if enough people accept that gender is different to sex at birth. This doesn’t mean we adopt whatever crackpot idea extremists propose, but what people believe changes through time. What is currently acceptable is called the Overton Window and politicians know the best way to move it, is to speak from just outside it.

Scientific explanations require repeated testing before acceptance. Non-scientific explanations are about shifting the consensus towards a new way of thinking. They are not right or wrong, but accepted.

The Dismal Science

Economics is the dismal science. This snobbery stems from a belief in a hierarchy of explanations. When physicists split the atom they find lots more to investigate. Researching electrons, protons and neutrons reveals quarks. Explaining the world at an invisible level is considered true science.

Good explanations are context specific. You cannot explain world events by reference to particle physics. David Deutsch provides an excellent example.

There is a bronze statue of Churchill in Parliament Square. It stands because we honour wartime heroes in this way. The explanation for how a copper particle got to the tip of the statue’s nose is meaningless without the context of history. Bronze is made from copper (and tin) formed from hot sulphur deposits in volcanic regions. Its particles behave in a certain way. That’s not why there is a statue of Churchill.

Whether we call explanations of events science or something else matters little. How acceptable the explanation is, matters a lot. Economists who turn their discipline into mathematical puzzles in an attempt to be like physicists, find their explanations suffer as a consequence.

An economic model requires assumptions. These might be that individuals are rational, an economy is closed (like North Korea), or two countries trade only with each other. Assumptions need definitions, such as what rational means. The more assumptions, the less the model reflects the world. Regardless, once accepted it is used to make government policies.

“Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist.” – John Maynard Keynes

Politicians want outcomes, such as income equality, and embrace models that predict it. Evidence is not necessary that the models work; an academic seal of approval is enough. When policies fail, politicians say “we didn’t do enough of it” rather than “we were wrong”. The rest of us end up in giant experiments with too many moving parts to know what causes anything.

All the leading Wall Street economists failed to predict what would happen when the Federal Reserve hiked interest rates. Their models said there would be a recession. There wasn’t.

Analysts model how the stock market works from theories. These are coded into algorithms that trade at lightning speed. While the assumptions of the model hold, the trades are successful. Then they stop working.

Traders accept this. Quantitative analysts constantly update algorithms. They don’t seek perfection because it doesn’t exist, but rather new explanations of evidence. They expect change and adapt accordingly.

Some investors remain stubborn. “In the long run this will happen,” they say. If you don’t define the long run you are never wrong. The worst kind of stubborn are value investors.

The Intelligent Investor

Benjamin Graham published “The Intelligent Investor” in 1949. A 20 year-old Warren Buffett read and adopted it. At the time, over three-quarters of US shares were owned by individuals. They invested for emotional reasons such as family ties or familiarity with brands, or for speculation. Graham spotted his opportunity.

Graham devised a way of finding shares that subsequently did better than the Dow Jones Index. He sought “an earnings ratio twice as good as the bond interest ratio”. His formula captured growth, management quality, financial strength and dividends. It tested well over fifty years of data.

Buffett defines intrinsic value as what a stock is worth. When this is above a share price he buys. When the shares rise towards his value he sells. He explains what intrinsic value means, but does not share numbers. His strategy depends on others following him.

Every share traded is bought and sold, but someone makes a price. When buyers are more urgent they are less sensitive to price, and sellers set a higher value for shares. This urgency is called the flow.

Investors copied Graham and Buffett’s thinking and academics published papers about it. More money chased the ideas and this flow validated the thinking. Graham and Buffett are the heroes of value investing. Their success is one reason why institutions not individuals own most of the stock market today. Conditions have changed.

Share prices move all the time and there is no such thing as the right price. When some investors think the price has risen enough they sell. Momentum shifts and the price goes down.

Buffett made his billions by staying invested. Share prices rise through time. He long since changed his strategy and buys whole companies, bails out banks and deals with governments. Most of his money has been made at an age when others are retired. This is just maths.

Picture a billionaire whose wealth doubles each year. The previous year they had half a billion and the year before a quarter. Three-quarters of their wealth has come in two years. When share prices rise by a percentage, all the owners benefit. But in pound or dollar terms, the ones with more invested make the most money. The rich get richer.

There are many explanations for why share prices rise. Company profits grow and their shares are worth more. The supply of money rises and some of it flows into stock markets. People earn and invest more as the economy expands. All reasonable but imprecise.

Boomers and Millennials

Graham’s legend received a huge boost from the boom in the post-war pension industry. Pensions had been provided since the Bureau of Pensions was established in 1832, but became widespread with tax breaks in the 1940s and ‘50s. This led to a boom in the mutual fund industry.

Mutual funds are known as unit trusts in the UK. They allow small savers to buy many shares in one investment. Thanks to theories that owning many shares is less risky than holding a few, and that it’s hard to beat professional investors, individuals pour money into these funds.

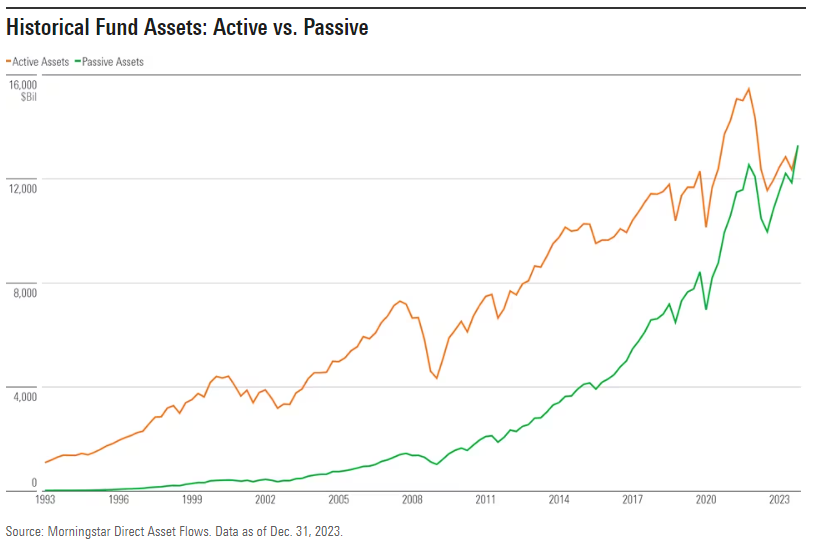

Mutual funds are superseded by Exchange Traded Funds (ETF) which have risen in popularity post the 2008 crisis. ETFs are tax advantaged, trade at all times of the day and have lower fees. This is often because they track the market or a segment of it, rather than paying a fund manager to choose investments.

ETFs hold around 12% of US shares, while at least a third are in mutual funds. Boomers own mutual funds and Millennials ETFs. Boomers are retiring and selling, while Millennials’ income grows and money flows into their pensions. Gradually ETFs will overtake mutual funds and index tracking replace fund managers selecting shares.

Indexing is called passive investing. The arguments in its favour are lower fees and better returns than most actively managed funds. It’s also important that low-cost funds are the default option for 401k plans provided by US employers. Company executives are obliged to find the best option for employees. Lawyers interpret this to mean the lowest cost. No boss will go to jail to try and increase workers’ pensions.

UK and European markets favour more expensive, active management of pensions. Ironically this has meant choosing to buy US shares for the last two decades. This matters because of the role of stock markets.

The Invisible Hand

Why do we have stock markets? One reason is to allow owners of private businesses to raise money. While they could sell to another company, better prices are available on public markets where more money flows. The bigger the market, the more companies it attracts.

Another argument for stock markets is capital efficiency. The wisdom of crowds means money flows to the good companies and away from the bad. The bigger the crowd the greater the efficiency. Adam Smith called something similar the invisible hand of the market.

But passive investor aren’t wise. They buy what is already big and make it bigger. Followers of Graham and Buffett bemoan broken markets. What they really mean is their methods no longer persuade enough people to follow them. Their explanation for why share prices go up and down is no longer accepted by the majority.

Private markets are more efficient than stock markets. Hence more money is flowing to them. But private investments are off limits to most individuals, who must rely on their pension manager to buy exposure. Rich individuals may invest directly.

Once the winners in private markets are established they list on stock markets and everyone can buy. Prices rise because of the flow that new shares attract. Just like Buffett, the game is to buy before a new surge of money flows into shares. Moving up the food chain into private markets means being earlier in the queue. Investing works if you buy before others.

Making a Fortune

There is hope for the dwindling number of managers selecting shares on public stock markets. The theory is that the more flow that is passive, the less purchasing power is required for some shares to outperform.

Imagine two companies of the same size that everyone owns. You are the only investor choosing which to buy. You prefer company A and put all your money in it. Next month, more of everyone’s money flows into company A because it is slightly bigger. This continues month after month and owning company A makes you rich and famous.

Let’s call company A, Nvidia. This company makes the chips powering AI and released results last night ahead of analysts’ predictions. The share price is following a similar path to that of Cisco during the dotcom boom.

This comparison lacks context. The graph implies a relationship without explanation. But explanations are just what most people believe.

Why not program an algorithm to trade Nvidia as if it were Cisco? The more investors who follow your thinking the more you are right. Index funds follow your lead, supercharging returns.

Value investors say it’s mad to pay 20 times sales for Nvidia. In time they may be right, not because they are smart, but because someone becomes urgent to sell.

That someone may be using this chart and have already programmed the machine. By sucking the most money into Nvidia before they sell, they stand to make a fortune.