The World Sails into a Storm

There’s no recession and markets are rallying. What could possibly go wrong? It’s time to take The Sniff Test.

An Era is Over

Two weeks ago the financial world roiled in a storm. Many in the West paid scant attention, as Kamala Harris inherited the Democratic nomination, Paris parked its political problems to host the Olympics, and the UK media cooked up a crisis. Yet the commotion was merely a warning.

Financial storms break in August. Senior investors are on holiday, trading is quiet and adverse news has outsized effects. This creates conspiracy theories about market manipulations. By September, when serious people are back at work, calm is restored.

Each of the world’s three largest economies is desperate to unleash liquidity. The US requires the stock market to rally into the election. The Chinese want to accelerate growth and Japan must correct the imbalances of 25 years of zero interest rates.

What everyone knows about markets takes an age to unfold. One by one investors shift positions, but at first few pay attention. Once a tipping point is reached, everyone resets and revisionists start explaining why change was inevitable.

The post financial crisis era is over, but most investors are yet to adjust. They know they must, but timing is everything. While there is a last drop in the lemon, then investors squeeze.

A Pinkie Promise

I write The Sniff Test to explain what I struggle to understand. All the theories I learned at university about foreign exchange seemed circular. It took years to realise that the concept of equilibrium is meaningless in a world of constant motion.

Say a country raises interest rates. Money flows into its currency and other nations must respond by raising rates. But rates rise to fight inflation, which is bad and means currencies weaken, so no one buys currencies with higher rates. Which is it?

Exchange rates fluctuate all the time. There is more trading in foreign exchange than any other asset. The world is complex and any model of it must be a simplification. As a result, it doesn’t work like the real world for very long.

Japan began a zero interest rate policy in 1999. The chart shows that the seismic shift in its currency was the strengthening from 1971 when the US came off the gold standard. By comparison, this century’s undulations appear uninteresting.

The important element of the chart is at the bottom. This shows the volume of trading in dollars versus yen. It increased after the financial crisis and surged after 2015 and again in 2023. It is the amount of money betting on currency movements that makes even small changes matter.

The Japanese authorities are in a slow dance with reluctant investors. They seek to lead, to nudge towards change, but investors drag their heels. They are comfortable with the current moves.

This changed on Monday of last week. There was a panic across currency, bond and equity markets. The Japanese stock market had the worst day since 1987. This was triggered by interest rates in Japan rising to 0.25%.

You read that right, 0.25%. That’s 5% lower than rates in either the UK or US. Borrowing money in yen, and lending or investing it in dollars, is a sure thing. Lending in currencies such as the Mexican peso makes more, but the size of the yen and dollar markets mean they are the ones that matter.

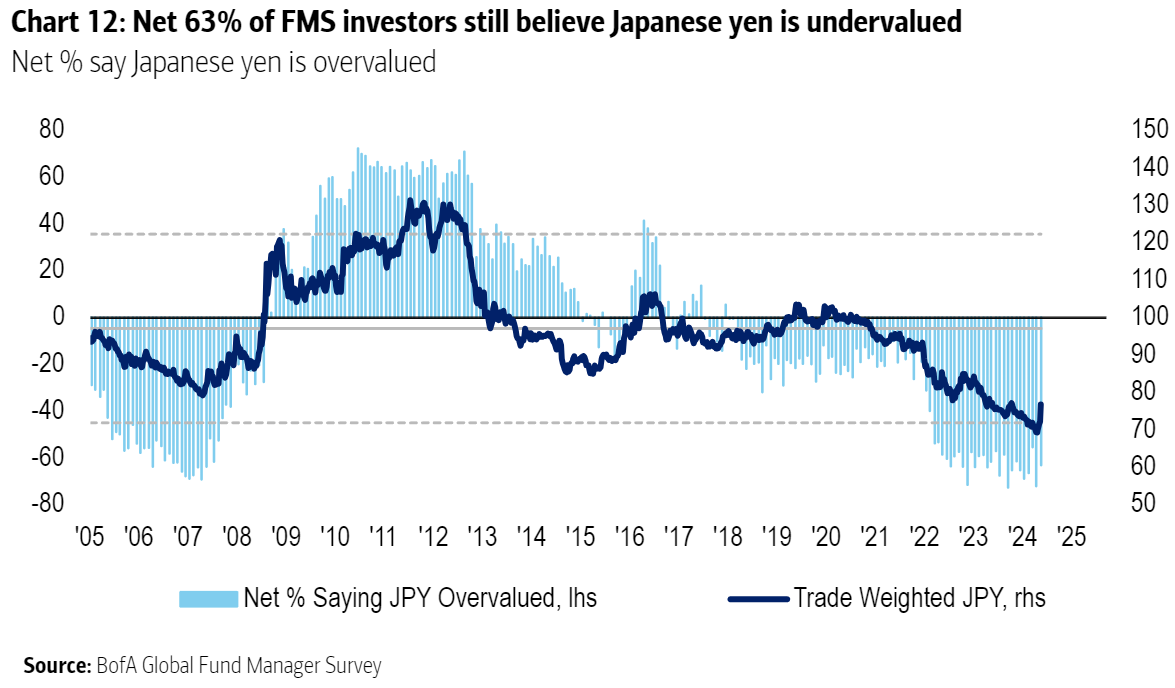

The majority of investors say the yen is undervalued. This should mean they expect it to strengthen as Japanese interest rates rise. Yet having frightened investors on their summer holidays, the Bank of Japan made a pinkie promise not to do so again this year.

In theory, the serious investors have from September until year end to sell international assets and repay yen loans. In practice, they know nothing new is happening. That means there’s plenty of time to keep making money.

A Homegrown Explanation

US capital markets are the largest in the world. Some think Americans are parochial. I’ve met a lot of US investors who’ve never been to Europe.

Last Monday, US markets fell by the most since 2022. The revisionists got to work imagining a US centric reason for this. Unemployment numbers had been a little worse than expected the previous Friday, so Reuters ran the headline:

Nasdaq, S&P 500 fall 3% each amid US recession fears, Apple drop.

The response to a recession is always lower interest rates. Hence investors bought bonds, which means the interest yield on them declines. This anticipates the Federal Reserve cutting formal rates.

If dollar interest rates fall between now and year end, it will be less profitable to borrow yen and lend in dollars. In theory, having received a warning of what might happen, investors will unwind this trade in an orderly manner.

In practice, lower interest rates to stave off a recession, mean US markets remain attractive. There’s plenty of time to make money.

Juicing the Returns

A 5% return from borrowing yen and lending in dollars is a bit dull. If you are going to the trouble of setting up this trade, then you want a little more juice. Having borrowed yen to buy more in the US, you now need low risk leverage in US markets.

A low risk, low return trade is said to have low volatility. Serious investors target a return and then borrow lots of money to super size bets. Say you want to make 8% a year. You set up a 2% return trade and borrow enough to make it four times bigger. The big money managers are huge borrowers.

This is what UK pension funds were doing when Liz Truss rolled into Downing Street. The sudden spike in UK interest rates made borrowing much more expensive and left many funds technically insolvent.

In theory, you wouldn’t want to do that again. In practice, the Bank of England bailed you out with lots of cash and Truss got all the blame. As long as you assume they’ll be a bailout, there’s still plenty of time to make money.

Options are a means of trading with borrowed money. For a small down payment, you get big exposures. If you buy options the most you can lose is everything. It’s like placing a losing bet. If you sell options however, it’s like being the bookie when the firm favourite wins a race. You lose a lot more than the value of the bets you collected.

Options are more complicated than horse racing bets. Lots of things influence option pricing. One of the most important is volatility. This means how much the price of an asset moves while you own an option over it.

The S&P 500 is the world’s largest stock index. It combines the value of 500 US companies (it’s 503 for odd reasons). Some go up, some go down and there is an average return.

In theory, when you buy an option on the price of the S&P 500, you are exposed to the aggregate volatility of the 500 companies. This should be equivalent to buying similar options on each of the companies’ shares. Except that it’s not.

Lots of people buy options on the S&P Index. This means you can sell in a hurry. This is called having liquidity and S&P Index options are a liquid market. As a result, there is a limit to how much the price of the options moves, meaning they have limited volatility.

This is not the case for each of the 500 companies in the index. Options on some of the shares are in short supply. If you want to buy a lot of them, the price may move a lot. In other words, the price is volatile.

All of this means if you sell options on the index and buy options on the individual shares you own volatility. This is called being net long. Volatility is valuable and hence you make money. In theory this opportunity does not exist, but in practice it does due to the structure of markets.

Does the sudden drop in US markets mean the economy is about to enter recession? No, leading economic indicators are improving, the business cycle appears to have bottomed and small businesses remain optimistic.

One reason that US stock markets fell 3% is because investors who borrowed yen made complicated bets in US option markets. Because you can lose a lot of money trading options, these investors are on a hair trigger.

Imagine race sailors making a yacht go as fast as possible. They throw their weight to one side to counter the powerful forces pulling the other way. A freak gust could tip them over, and they know that the tack will end and they must shift sides. But until that moment comes, they lean over as far as possible.

August 5 was a strong gust. The boat roiled but stayed afloat. Now it’s back to leaning over the side.

Holding Course

Kamala Harris assumed the mantle of incumbency and in several polls established a slight lead over Trump. The financial establishment favours continuation over change and does not want to rock the boat. It would rather a stock market rally than a crash.

Lots of liquidity makes markets go up. When investors believe they can exit in a hurry, they are emboldened to take more risk. Arthur Hayes makes the case that the establishment will do a lot to ensure higher liquidity into the year end.

Despite trade wars and territorial spats, the US talks with Japan and China. Japan wants to sell dollars and buy yen. The dollars it sells will need to be invested somewhere. US capital markets are the default option.

China wants to stimulate its economy by providing liquidity in local currency. It needs a weakening dollar to ensure the value of the renminbi does not fall. The US commits to lower interest rates to facilitate this. Liquidity rises everywhere and everyone gets what they need.

Investors play along and in doing so, exaggerate the trends. You always borrow aggressively when there is a low risk bet. This stores up trouble.

A weaker dollar and stronger yen would reverse the one-way flow of money over the last decade. No one knows how much has been bet this way, but it’s a lot. Hayes cites Deutsche Bank research to estimate gross risk of $24 trillion. In theory, much of that is hedged, meaning one risks offsets another. Practice is another thing.

Liquidity will be necessary beyond the election. Moreso if the victor fulfils promises to spend. This will be debt funded and the major economies are already heavily indebted. The nature of debt is that it needs refinancing. As a result, central bank’s primary role has become funding of new government debt, rather than looking out for inflation and unemployment.

Investors know this and structure trades to benefit. The longer the situation persists the more they are emboldened. The authorities must stay the course.

For years the Japanese borrowed money, injected liquidity into the economy and allowed the yen to weaken. Japan’s ageing population is deflationary and offset this. The paltry returns on domestic assets were more than made up by foreign investments, notably in America.

Eventually, all that liquidity triggered inflation. It’s nothing like the levels in the West, but serious enough to require interest rates above zero. Even a slight rise in Japanese rates signals the end of an era. It’s time to start shifting to the other side of the boat.

Yet first there’s an election to win. The skipper holds course for just a while longer. Someone’s getting wet, but serious investors believe it’s someone else. For now, there’s still plenty of time to make money.

Excellent piece to read thank you about an area of financial markets where the dark arts are marginally more nefarious than the front rows of an All Blacks v Springboks scrum

As well as monetary policy across the Western economies, I’ve also been watching the volatility in Gold, Silver and crude oil (especially the Brent future contract which is cash settled unlike WTI) and to echo your point about the purpose of rate hikes, much is entirely counterintuitive

The inflation we have now was almost certainly a direct consequence of government policies locking down economies and, as Mervyn King pointed out, the concomitant issuance of furlough creating too much money chasing too few goods This has been compounded as ’til death us do part’ commitments to net zero coupled with inflation busting public sector pay rises more or less echoes the point Kalecki made in 1943 https://www.exploring-economics.org/en/discover/political-aspects-of-full-employment/

So central banks using the monetary sledgehammer to crack the supply side inflationary nut looks to be a deliberate misdiagnosis?

A recent podcast between Tom Luongo and Vinci Lanci

(https://tomluongo.me/2024/08/02/podcast-episode-186-vince-lanci-and-how-davos-manipulates-time/)

makes the point that we cannot ignore unprecedented levels of Western government debt vs the poor growth rates which markets have yet to make a serious consideration of the prospects of sovereign default risk which may explain why the Bank of England have been manipulating an inverse yield curve, and the ECB manipulating credit spreads as evidenced by the massive UST buying since 2021 when Powell started to raise rates (which has reduced the size of the offshore dollar market, as China started to sell

So was Truss ousted in a BoE led coup because what she proposed exposed the above also when Janet Yellen is at odds with Powell who refuses to lower rates resulting in a stealth QE via short dates debt issuance ?

Which brings the discussion to commodities notably Gold which has rises sharply in the last two years despite ‘higher for longer’ yields and strong equity markets The purchasing of Gold by China and Russia has certainly shifted the deliverable Gold market east and Comex has reacted accordingly

Also noticeable is the massive manipulation of crude prices via the Brent contract (last week of May/first week of June) as put options around the $80 and $79 strikes were taken out and move the spot price down 5% in three days

Who needs the price of crude oil weaker ?

Who needs dollars to prop up its weak financial system ?

All the counter intuitive volatility across asset classes points to significant stress somewhere in the Western system which they are expending vast capital (actual and political) to stop

It points to the Eurozone which makes the November election crucial for each faction involved