What This Year’s Elections Should Be About

Voters care about who pays society's bills. It’s time to take The Sniff Test.

An Election Issue

In 2006 the FT published my letter predicting a banking crisis. I was not alone in this and not all my predictions work this well. I did not foresee this uprooting the post war political consensus.

I wrote about debt here and here. I am writing now about its impact on business and consumers, because this should be the election issue. Whoever wins, governments will spend more money. For 80 years this has dampened economic cycles. For 65 of those, business and consumers responded together. This is no longer the case.

Any prediction about unsustainable debt is speculative. The future is uncertain. But what benefited government, big business and consumers now boosts only two. Households and small businesses are suffering. This will impact elections for the foreseeable future.

Calming Down Capitalism

This chart shows two measures of the US economy back to 1875. The top graph is real GDP growth, which measures how much the size of economy changes after deducting inflation. The lower is the GDP deflator, which is inflation.

Both graphs divide into two distinct periods, before and after World War II. Before the war the economy went through rapid cycles of boom and bust unknown to most of us alive today. These were accompanied by bouts of rampant inflation and then price collapses. A word for this is unpredictable.

Since World War II economic growth has been stable and on a modest downward trend. The deep recessions around the 2007-8 financial crisis and Covid, were mild compared to what used to happen. Things have calmed down. Why?

The earlier period is referred to as laisser-faire capitalism. The government did not intervene much in the economy. Income tax, for example, was only introduced in 1913 at rates of 1 to 7 percent. When business boomed it really boomed. When the bust came the marginal companies went under, alongside the banks that lent to them. The slate was cleaned.

From one perspective this was a good thing. Excessive borrowing and poor business decisions were punished and bad practices eliminated. Yet there was significant human cost in terms of mass unemployment, destitution and depression. The Great Depression of the 1930s proved too much and Franklin D Roosevelt set about making sure it never happened again.

There are many twists to that tale. FDR had to overcome entrenched opposition from powerful business interests. As a Democrat, he had to compromise with the racist Southern element of his party. This delayed reform of civil liberties into the 1960s and the next big Democratic government intervention of the Great Society. Yet FDR achieved his aim of legitimising massive government spending.

John Maynard Keynes is considered the author of government deficit spending. His seminal work “The General Theory of Employment, Interest and Money” was published in 1936, when FDR’s New Deal was underway. The work develops Keynes’ earlier thinking and recommendations, and was mirrored in FDR’s policies. We don’t know how much influence Keynes had on America at the time.

He would become a huge influence. The book rocketed Keynes to international celebrity and justified government intervention in economies until the late 1970s. Then Reagan and Thatcher’s monetarism took over, inspired by Friedrich Hayek and Milton Friedman.

Returning to the chart, we see the immediate success in dampening and stabilising economic activity and inflation. But governments ignored a key tenet of Keynes’ theory. While they spent to offset the bad times, they refused to save in the good. Debt built up across the economy. For a while this worked.

Preventing sharp downturns means not all bad businesses go bust. Some excessive borrowing remains. Bad lending by banks is only partially punished. In time, people adjust to the idea that excessive speculation is subsidised, provided you are important enough.

Spoils of War

Issuing government debt removes money from the private sector. In downturns this does not matter, because people and businesses are scared and don’t spend. They buy government debt to shelter from the storm.

Governments must spend the money they raise to rekindle economic growth. Keynes’ assumed they’d invest in roads and bridges, scientific research and long term projects that the private sector shied away from. The money funded valuable assets that would otherwise not be there, as well as offsetting private caution.

There was supporting evidence. The US ramped up spending during World War II and the economy boomed. It fell into recession as spending retreated in 1945.

Military spending delivered major technological advancements. Radar was new enough at the onset of war that the British establishment refused to accept the Germans had it. By the end, both sides knew how to jam and deceive radar.

The Allies fooled the Germans into believing a large fleet was approaching Calais ahead of D-Day. Radar boosted civil aviation, marine navigation, meteorology and microwaves after the war.

Other spending encouraged business to embrace science. There were advances in synthetic rubber, plastics, medicine, computing, jet engines, nuclear power and space travel. Ancillary benefits proved just as important, such as the development of logistics and moving goods and machinery over long distances.

The US benefited more from military spending as the war took no toll at home. The indebtedness and damage inflicted on Europe took longer to shake off. But once again it was the pull back in government spending that caused recession in the UK, rather than the war.

In France, ravaged by fighting and without effective government, the economy collapsed until spending resumed post war. Everyone learned the lesson that government is good.

The belief that government spending boosts both short and long term prospects is engrained in politicians and bureaucrats. It no longer matters what money is spent on. While the private sector seeks productive investments, politicians fund pet projects.

The monetarist revolution of the 1980s changed the tools but not the concept of benign intervention. The virtuous circle lasted until the crisis of 2007-8.

Consumer Borrowing Booms

Government intervention prevents bad debts being wiped out and keeps weak managers in business. The price is worth paying to protect individuals from depression. It means that each post-war cycle adds a layer of debt.

Governments do not save in the good times. This means each bout of spending adds to the deficit. As the earlier letters debated, the jury is out as to whether this matters for the overall economy. But macro economics is insensitive to the plight of people. Debt has a large impact on individual behaviour.

The post war recovery was a period of rising debt all round. Increasing confidence, liberalisation of banking and rising prosperity enabled more consumer borrowing. This culminated in a massive blowout of personal debt in the US housing bubble 20 years ago.

The chart shows consumer borrowing as a share of household income on the left hand side. This rose from under 90% to almost 140% in the 18 years from 1990. I talked last week about the feelgood factor accompanying the last Labour landslide. This was part of an international swell of optimism and is unlikely to be repeated.

The party ended in 2008. A generation is scarred by the experience. Despite almost zero interest rates from 2009 to 2017, there was no new consumer borrowing boom.

Something similar happened to small businesses, shown in the right hand panel. This measures how many borrow rather than how much. Owners avoided the mortgage blowout, but still chose to borrow less when rates were nothing.

Covid is an anomaly on both charts. This was a period of massive expansion in both money and spending. All it did was get households and small businesses back to where they were. In the past this scale of spending unleashed a wave of optimism and consumer borrowing. Not any more.

This chart sums up the post pandemic change. For those reading on a phone, the lighter blue line is consumer confidence based on money in the pocket. The darker one is an assessment of business and employment. They move in tandem for 43 years and fall apart after 2021. Consumers know there are jobs and opportunities for business, but they no longer believe they will benefit.

This is what this year’s elections should be about.

There are no unbridled market forces in the post war period. Economic debate centres on the degree and methods of government control. Politics worked because more debt boosted both business and consumers. This is no longer true.

A Blank Cheque

Since 2008, the US government has bought or guaranteed most mortgages. Covid relief programmes forgave business debts. Student loans are dismissed. Yet individuals are not appreciative and politicians don’t know why.

Each of these developments swaps private debt for government. Bank bailouts do the same. The excuse is protecting depositors. This was limited to smaller amounts, but has been extended to cover all sums for fear of panic. A mere mention of downturn is enough to enact any amount of intervention.

Geopolitical tensions trigger the same response. The private sector will not reshore manufacturing without subsidies, so a blank is cheque is written. The left calls this going green and the right resisting China. Either way it’s more debt.

Government debt is different to yours and mine. Taxes may be raised, financial companies forced to buy bonds and central banks absorb what’s left. Inflation can be stoked to erode debt piles and currencies adjusted. These all have costs.

We feel it now when taxes are hiked, inflation rises or the price of the pound falls. We feel it tomorrow when our pensions come up short because they are stuffed full of debt. Every political party promises a combination of the above.

We have reached a tipping point. When governments intervene there are always losers. When most people win then spending works. Not enough of us feel the benefits any more.

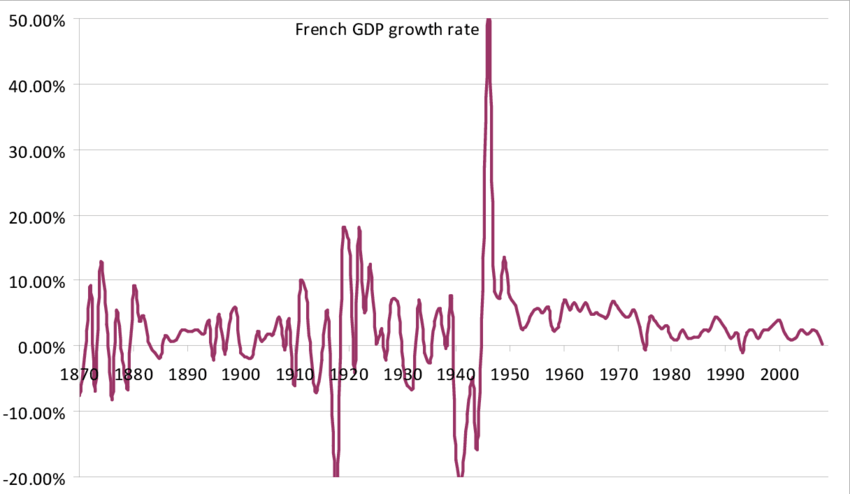

A similar thing is happening at country level. Latin America went bust in the ’70s, South East Asia in the ’90s and the European fringe last decade. Japan will be broke if it raises interest rates. The fear that France will follow spooks markets after Macron called an election.

The Last Domino

In the post pandemic period the US attracted one third of all global capital flows. America will be the last domino to fall. It will take until 2060 for its interest costs to reach a third of government revenues, which many consider unsustainable. Until then, the dollar sucks up wealth like a giant milkshake.

It’s a feature of dollar dominance that the US attracts more money during panics. It’s the safest place, even when its ferments a crisis.

The standard response to a crisis is to create and spend money. The rescue act used to encourage banks, companies and consumers. No more.

Those who can afford to borrow are ageing. Their consumption is falling. Younger generations are scarred by student loans and cannot afford houses. They neither marry nor breed, two things that loosen purse strings. Their inheritance is a debt mountain that no longer works for the majority.

The resolution is not obvious. It’s easier to predict problems than come up with solutions. My assumption in 2006 was we’d struggle through the consequences of a banking crisis. Governments responded with unprecedented intervention and for a while things looked good.

Consumers felt better off but did not borrow to spend as in previous decades. When Covid came governments changed tack and gave us money to spend. People spent but are not stupid. We know there is a price to pay.

Elections should be about who pays and how much. Right now voters believe it’s all on them. That’s why the polls in the UK and US say the incumbents will lose.

How is the situation resolved? I think (and of course I may be wrong), that the real economic crime of the last couple of decades was not government spending per se, but rather the enthusiasm of central banks to pursue zero or near-zero interest rates and, at the same time, distort long-term bond yields by sucking up the paper. This allowed triviality and corruption to flower in many ways, crucially including corporate behaviour. Managing a business well is hard and dangerous; congratulating yourself for making your employees undergo DEI and/or SGE indoctrination is easy. To that extent, management was granted the privilege of entertaining themselves with displacement activity, rather than the tough work of management.

If we have seen the back of ZIRP/quasi-ZIRP, then this displacement activity will no longer be survivable - markets will simply replace the trivial/corrupt/decadent management cohort we have bred. It's been done before.

And if so, then the answer to how we fight back from our present condition is easy and old-fashioned: we re-discover the magic of compounded small gains. In other words, prey for grey normal days, and vote for anyone who promises to do . . . very little extraordinary.

I’ve never had a letter published in the FT, but I did manage to get a letter published in the Independent in 2011 (known as the Indescribable by Private Eye) pointing out to Labour MEP Richard Corbett who said the best way to deal with the rise of UKIP in the EP was to defund them My main point was that this was monumentally stupid because a) UKIP had broken no rules and b) UKIP was supported by far more Labour voters than Tories A decade on and Corbett continued to occupy his bubble of delusion

Mark Blyth spoke extensively about why austerity is a bad idea

https://youtu.be/in5M65566iw?si=VmHXteNItZsgWiQk

What is interesting about his approach is that he like you acknowledged the bit of Keynesian theory the modern establishment likes to avoid and the ‘spend on anything as long as the government is spending’ is a recipe for collapse

The recent UK local elections and EU elections and subsequent calls of a snap General Election in the UK and France, looks a lot like panic to me In the UK a case can be made that the most seismic event was not the rise of independents in the local elections or even George Galloway winning Rochdale It was the fact that an independent candidate came clear second to Galloway with 6,000 votes in a parliamentary by election in a seat Labour regard as their own and typical of an area where the likes of Richard Corbett has no idea what is happening because the vote is taken for granted

It’s certainly the case the voters bought into Johnson’s aspirational manifesto of 2019 handing the Tories a majority they haven’t seen since Thatcher But yet again their aspirations are trampled over and whatever was promised was abandoned and the Sunak/Hunt combination took over and with no mandate increased government spending on God only knows what

With debt to GDP at 102%, a governing class ridden with scandal and nothing to show for it, Sunak will rightly be annihilated on July 4th But Starmer will form the next government as an unpopular leader for whom no one outside of St Pancras holds any enthusiasm for

It’s a similar story on Germany and France as AfD surge in the polls in the former and Marine Le Pen’s party looks set to form the next government in the latter Again it’s a reaction to an overbearing EU Commission that the CEO of Ericsson criticised for its obsession with regulation

https://fortune.com/europe/2024/04/30/ceo-sweden-biggest-companies-ericsson-regulation-europe-competitiveness-telecom-no-industry/

We on this side of the EU debate used the monicker EUSSR to describe its direction Seems we may be able to look back at that prophetic observation as Niall Ferguson provided a critique of Western (mainly US) policymaking

https://www.thefp.com/p/were-all-soviets-now

The voters have likely had enough